In succession conversations, valuation is foundational. It sets expectations and shapes what is possible. But the most successful transactions also depend on something less visible: why an advisor is buying or selling in the first place.

In the first installment of this series, we reframed succession as a lifecycle strategy rather than a one-time sale at retirement. This blog zooms in on the human side of that strategy: the motivations that drive advisors to buy, sell or pursue partial transitions, and why understanding those motivations is critical to deal fit and long-term success.

AssetMark’s 2025 Advisor Succession Survey shows that advisors rarely approach a transaction with a single objective. Instead, both buyers and sellers carry a stack of motivations, such as growth, workload, client fit, lifestyle and geography, that shape everything from deal structure to integration and transition outcomes. Quantitative factors like assets under management, revenue and valuation remain essential. They set price expectations and influence what deal structures are feasible. When advisors are clear about their motivations and communicate them early, they are more likely to find the right type of buyer and deal structure, and to negotiate terms that reflect what they actually want. When motivations remain vague or unspoken, even an attractive price can lead to friction, misfit or regret.

This dynamic is especially relevant in today’s market, where many advisors sell to institutional firms such as registered investment adviser (RIA) aggregators or offices of supervisory jurisdiction (OSJs), or use a sale as a partial liquidity event while joining a larger platform. In those scenarios, knowing what you want from the next chapter can matter as much as the economics of the transaction.

The survey reinforces this point. Advisors across age groups are actively pursuing different paths. Only 10% of advisors say their primary focus is selling or transitioning, while 42% are focused on growth through acquisition. Another 12% are open to either acquisition or sale. Motivations are not static, and they are rarely one-dimensional. Understanding and naming them is a practical first step toward better deal fit.

Seller motivation stacks are more than “time to retire”

Sellers are not a monolith. The survey shows meaningful differences between advisors pursuing full-book sales and those considering partial transitions, and those differences are rooted in motivation.

Advisors leaning toward a full-book sale tend to be closer to retirement, which is not surprising given that a full-book sale is often tied to a clean exit, emphasize goals such as stepping away from day-to-day client work, simplifying life and ensuring continuity for long-standing client relationships. For these advisors, clarity and finality matter. A clean exit and confidence in the buyer’s ability to absorb the book are often nonnegotiable.

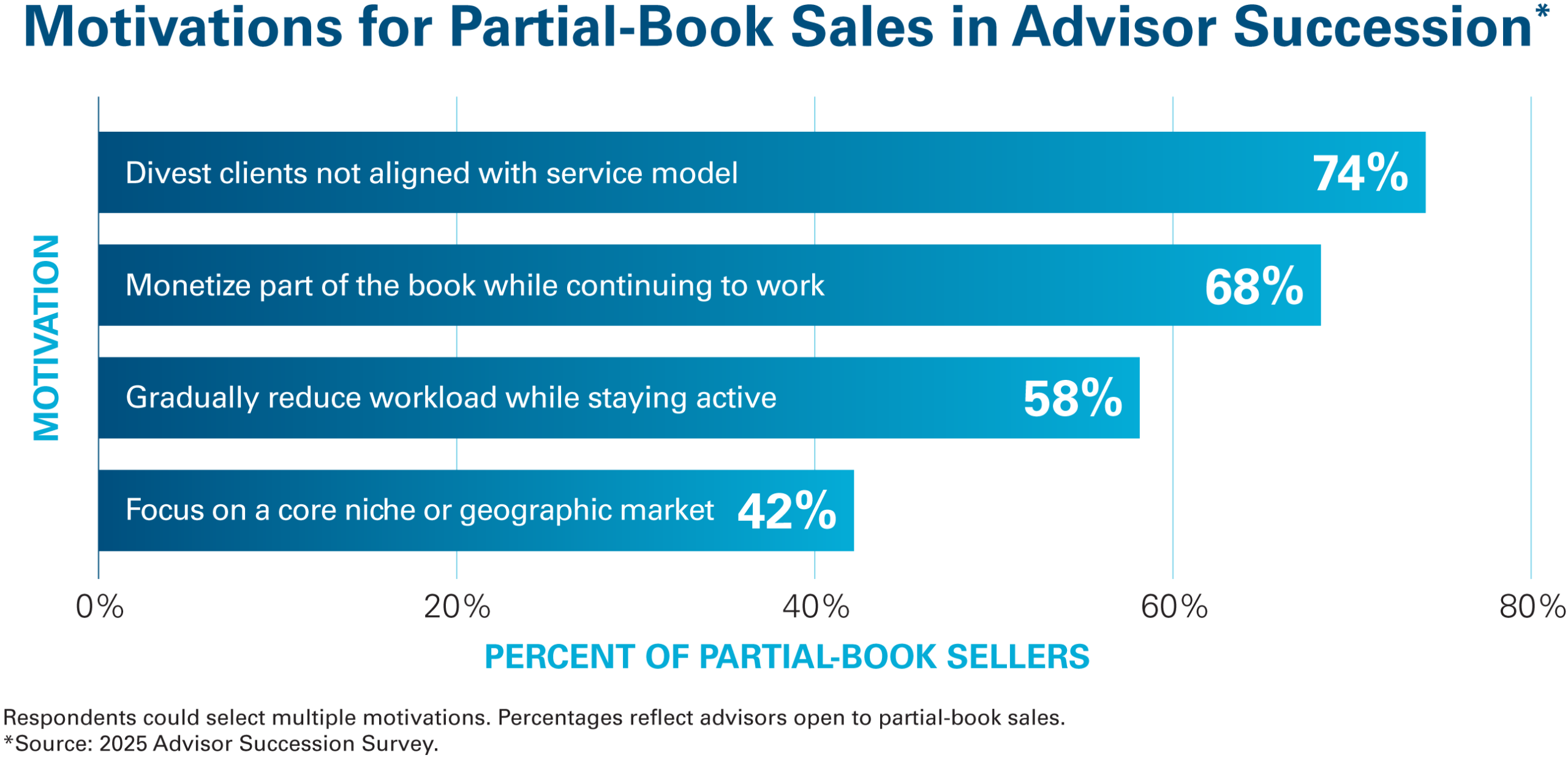

Partial-book sellers are typically not signaling indecision. They are optimizing for capacity, lifestyle and focus. The survey results below show that pruning misaligned clients and creating flexibility while staying active are the dominant drivers.

Most sellers select more than one of these motivations, creating distinct profiles.

A “sunset seller” prioritizes a simple, full exit. A “strategic optimizer” wants to reshape the book and business. A “lifestyle streamliner” is looking for flexibility while staying engaged.

Knowing which profile best reflects your situation, and which motivations are inflexible, is the foundation for finding the right structure and counterparty. That clarity also allows wealth management firms and other intermediaries to help identify buyers and deal structures that fit your goals and time horizon, whether that buyer is an institutional acquirer, an Office of Supervisory Jurisdiction (OSJ), a next-generation advisor or a peer practice.

Buyer motivations center on precision growth and strategic fit

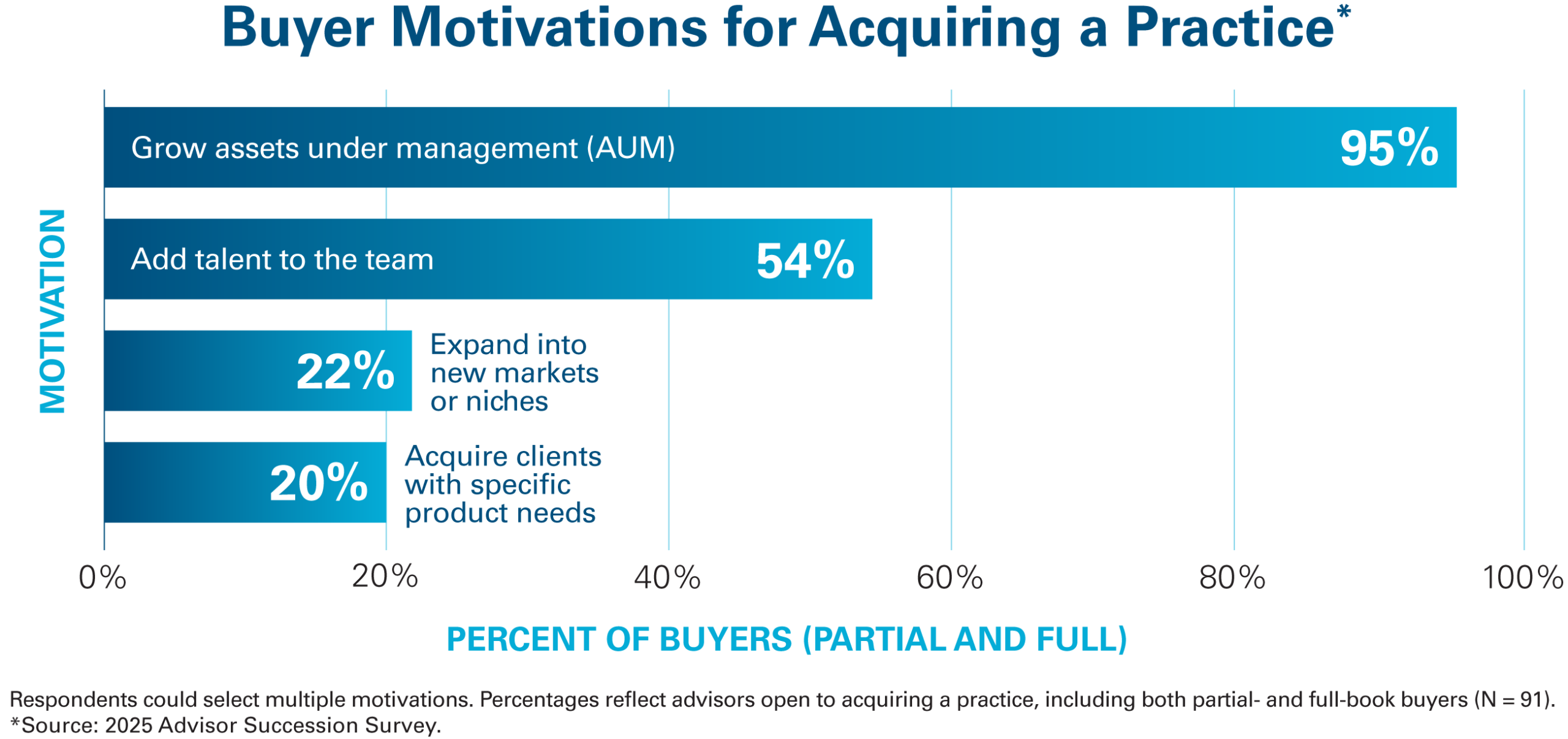

Buyers are not simply chasing assets under management. Their motivations are layered and often shaped by operational and capital realities.

Across the survey, buyers cite growth as a top priority, but growth is rarely generic. Many are focused on adding talent or next-generation advisors, expanding into specific markets or niches, or strengthening the alignment between acquired clients and their existing service model. These motivations show up across age groups, not only among early-career advisors.

In today’s market, many advisors sell to institutional buyers such as registered investment adviser (RIA) aggregators, enterprise RIAs and offices of supervisory jurisdiction (OSJs). These firms are built for deal activity and can transact at higher volumes, which can expand the range of outcomes available to sellers. For some advisors, that means a full exit and retirement. For others, it can look like a sale paired with a move to the acquiring firm as a partial liquidity event. In either case, understanding your motivations and preferred role after a transaction is essential to choosing whether an institutional buyer, a local peer or a successor advisor is the right fit.

Buyers also face real constraints. In the survey, 28% cited limited capacity to absorb an entire practice at once, which helps explain why partial-book acquisitions can be an attractive solution for many buyers.

Beyond capacity, buyers report a range of execution challenges that can affect any deal, including client transition complexity, valuation considerations and finding the right practice. Notably, about 80% of advisors who want to acquire say they have not yet found the practice they want , underscoring how challenging it can be to identify the right opportunity.

These realities create different buyer profiles. A “scale builder” focuses on adding assets and revenue. A “specialization seeker” targets clients within a specific niche or geography. A “talent and continuity buyer” prioritizes teams and long-term succession. Clarity around these profiles helps both sides assess fit earlier in the process.

Motivations shape deal fit and complexity

Different combinations of seller and buyer motivations create predictable patterns in deal fit, transition complexity and support needs. The goal is not identical motivations on both sides. It is a realistic understanding of what each party needs from the transaction.

A “sunset seller “paired with a “scale builder” buyer often lends itself to a full-book sale with clear timelines and a defined handoff. A “strategic optimizer” seller pruning part of the book may be a strong fit for a “specialization seeker” buyer in a partial-book deal that reshapes both practices. A “lifestyle streamliner” seller working with a “talent and continuity buyer” may require more creative structuring, such as staged transitions or shared service models.

When motivations are misread or unspoken, friction tends to surface later. A seller expecting a quick exit may struggle in a deal that requires years of transition support. A buyer seeking a narrow niche may be frustrated by a seller who expects whole-book treatment. Motivation profiles also signal how much guidance a deal will require. Mixed or complex motivations often benefit from one-on-one consultative support rather than general education or valuation resources.

What advisors can do now

Understanding motivations is not theoretical. It is a practical step advisors can take today to improve deal outcomes.

Start by defining your top three motivations for a potential sale or acquisition and ranking them. Build a simple motivation profile and share it with trusted stakeholders and intermediaries. Use motivations as a lens when evaluating opportunities. Does the other party’s profile complement yours? Does their firm type align with what you want for your next chapter? Will the structure and timeline support your goals, including how long you want to stay involved?

Naming motivations early will not guarantee a perfect deal, but it will make it far easier to identify true fit and avoid costly misalignment. In the next blog, we will build on these profiles to outline practical paths from exploration to execution, including how advisors can navigate partial and full transitions with greater confidence.

©2026 AssetMark, Inc. All rights reserved.

8751878.1 | 02/2026 | EXP 02/28/2028