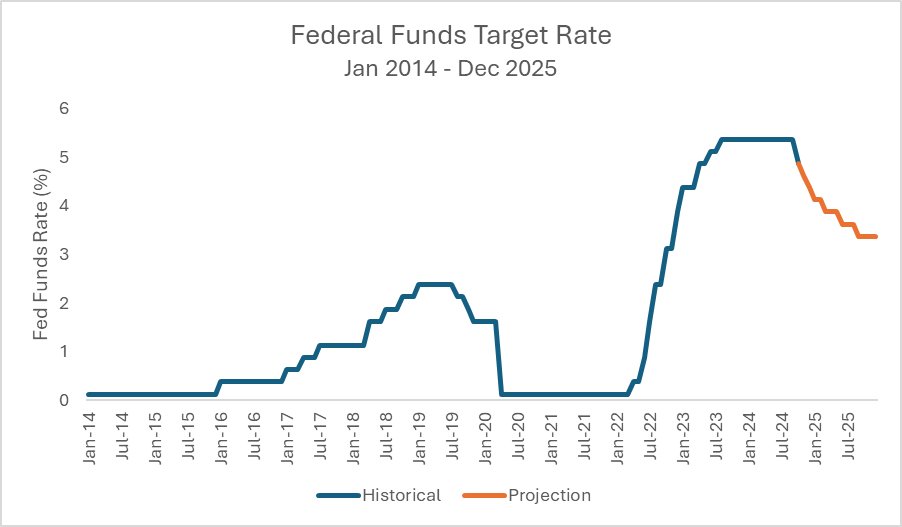

Over the past 2+ years the Fed consistently raised rates from a low of 0%-0.25% in the pandemic to 5.25%-5.5% by summer 2024. While this period of high and rising rates attracted a lot of client interest (and flows), it’s starting to come to an end. The Fed cut rates by 0.25% on November 7 and markets are expecting a number of additional rate cuts by the end of 2025.

So as an advisor, what does this mean? Does it impact how I manage my client’s cash? What should I be doing next?

Source: Historical: U.S. Federal Open Market Committee and Federal Reserve Bank of St. Louis, FOMC Summary of Economic Projections for the Fed Funds Rate, Median [FEDTARMD], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/FEDTARMD, October 15, 2024. Projections: https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

Advisor Response

The levels of your clients’ cash holdings will likely go down… a little.

In 2022, the average affluent client held 16.3% of their investable assets in cash and short -term investments. You’re unlikely to see much of a change in average affluent client’s cash levels. Why? Cash is an important allocation for most clients. They’re saving for a rainy day, saving for a down payment, or in cash temporarily after selling an asset. Most clients hold cash to meet their needs and goals, not to capture a high rate. While cash levels will rise and fall, it’s unlikely to move that much.

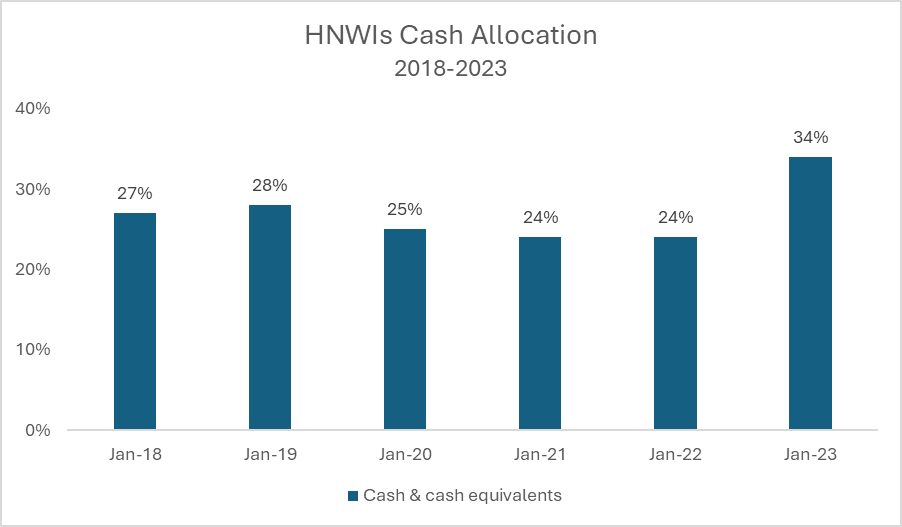

For HNW and UHNW investors, you’ll see more movement, but it will remain a major holding. HNW/UHNW clients tend to hold significantly more cash than affluent clients, with ~34% of their holdings in cash and cash equivalents in January 2023, up from an average of ~25% since 2018 according to a recent Capgemni report. HNW and UHNW investors’ cash allocations tend to be more rate sensitive than average investors due both to the size of the assets involved and a greater willingness to take a tactical approach to the market.

This is still a huge opportunity for advisors to consolidate SOW and improve client outcomes!

Source: Capgemini Research Institute for Financial Services Analysis, 2023

Planning is the key to effective cash management

Clients often focus on finding the “best” (i.e., the highest) rate. However, with impending rate cuts, the rates available today are going to start to come down, potentially quickly. Different cash/short-term products will pass through rate changes at different rates.

You can help your clients by doing some simple financial planning. First, identify “buckets” of cash like an emergency savings fund or funds for a large purchase. Then for each bucket, determine when your clients’ needs cash. While clients may have different risk levels and investment options, they often don’t have flexibility on when cash is needed. This especially matters in a declining rate environment. For example, consider a client that has $100k and needs the cash in 3 years. They can invest in a money market fund paying 5% or a CD at 4%. Which is the better investment? While many clients will lean towards the 5% rate, if rates decline significantly, clients will probably earn more with a CD.

Evaluate if it’s time to invest some of the cash in the market

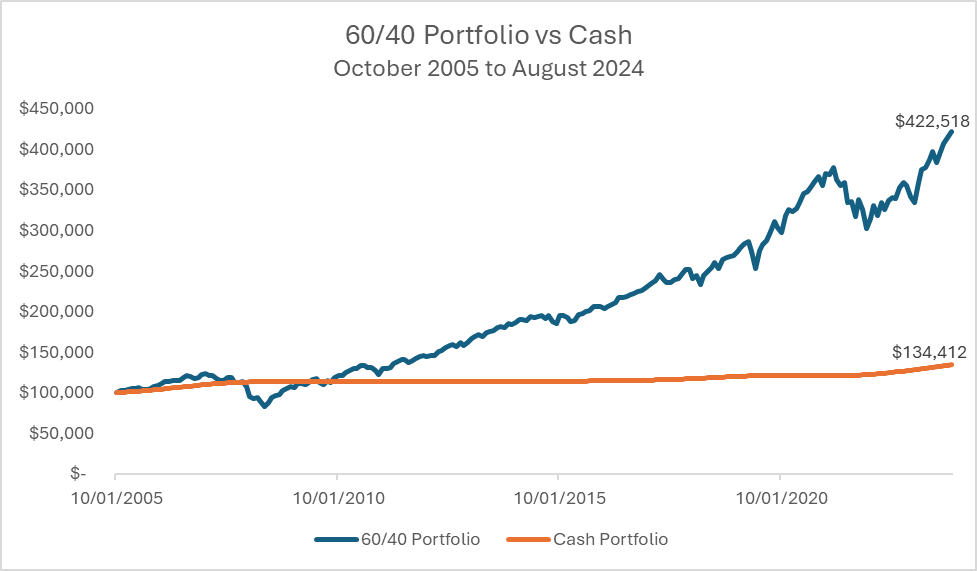

If your clients’ goals are long-term, evaluate if they are holding too much in cash and highlight the risk to their long-term financial well-being – namely by being in cash they limit the potential for short-term losses, but bypass potential, long-term stock market investment returns.

Source: Zephyr. Historical Returns for US Blend (S&P 500 60%; Barclays US Agg 40%) and US T-Bills 1-3 months

7275771.1 | 11/2024