As the year draws to a close, many clients enter the traditional “giving season” with an eye on both their financial plans and their charitable goals. Year-end is a prime time for financial advisors to help clients review their philanthropic priorities and maximize available tax benefits before December 31st. This planning is especially critical in 2025, which provides a window to expand client impact by aligning charitable intentions with smart tax strategy before new tax provisions take effect.

2025 Tax Law Changes: The ‘Big Beautiful Bill’ and Charitable Deductions

Legislation passed in mid-2025, dubbed the One Big Beautiful Bill Act (OBBBA), brings significant tax changes that affect charitable deductions. Advisors should understand these changes to guide clients effectively:

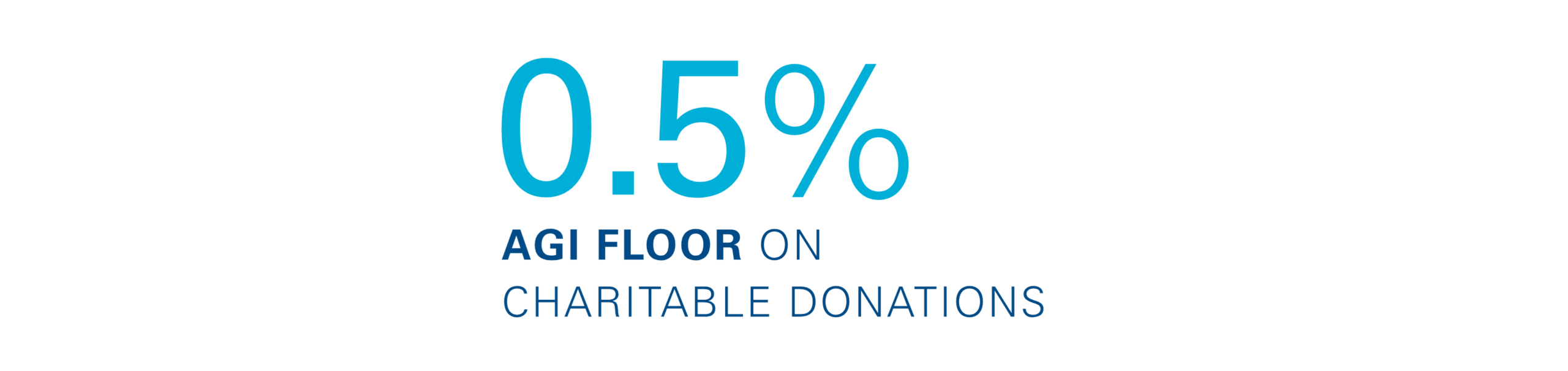

0.5% AGI Floor on Charitable Deductions (Starting 2026)

Beginning in 2026, itemizers will only be able to deduct the portion of their charitable contributions that exceeds 0.5% of their adjusted gross income (AGI).

In practical terms, a couple with $200,000 AGI would get no tax deduction for the first $1,000 of their donations; only giving above that $1,000 threshold would be deductible. This new floor means small or modest charitable gifts may no longer yield any tax benefit for itemizing taxpayers. The truly generous givers might not be deterred, but those on tighter budgets could respond by bunching donations into certain years to clear the 0.5% hurdle.

Crucially, 2025 is the last year without this restriction – so clients can still deduct every dollar of their charitable giving (up to normal AGI limits) on 2025 returns without worrying about a floor.

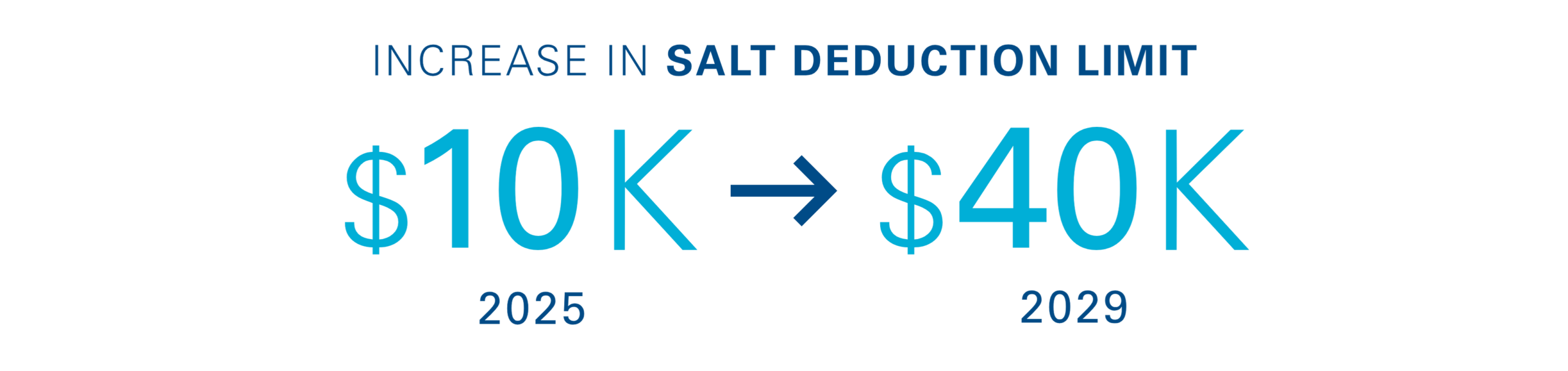

State and Local Tax (SALT) Deduction Cap Changes

The same law also delivered a temporary boost to the SALT deduction limit. For tax years 2025 through 2029, the cap on state and local tax deductions jumps from $10,000 to $40,000. This four-fold increase (phased out for higher incomes above $500k modified adjusted gross income) provides meaningful relief to homeowners and high earners in high-tax states.

It could make itemizing deductions in 2025 far more attractive, since many clients who were previously capped at $10k for property and state taxes can now deduct up to $40k. When combined with charitable contributions, a higher SALT cap may enable some clients to itemize in 2025 when they otherwise wouldn’t. (Notably, this expanded cap is temporary; it shrinks after 2029 and reverts to $10k by 2030.)

Advisors should consider the SALT change in tandem with charitable planning – for example, a client might pay two years’ worth of property tax by year-end 2025 (and itemize it) and then take the standard deduction in 2026.

Other Changes

OBBBA made permanent the higher 60% of AGI limit for cash gifts to public charities (originally set to expire in 2025), preserving the ability for generous donors to deduct large cash gifts in one year. It also slightly reduced the top marginal benefit of itemized deductions (capping it at a 35% tax benefit rather than 37%).

Additionally, starting in 2026, even taxpayers who don’t itemize will be allowed an above-the-line charitable deduction (up to $2,000 for joint filers, $1,000 single) – but donations to donor-advised funds (DAFs) and private foundations won’t count for that break. This means direct gifts to public charities get a small boost for non-itemizers, but DAF contributions remain beneficial primarily for those itemizing (or bunching donations to itemize in a given year).

Why 2025 is a Critical Planning Year

The upshot of these changes is that the tax landscape for charitable giving will tighten after 2025, especially for moderate-level donors who may be impacted by the new 0.5% rule. Advisors should communicate to clients that 2025 is the time to maximize charitable deductions under current rules. By acting before year-end 2025, clients can take full advantage of today’s deduction rules (and the temporarily higher SALT limit) to potentially reduce their 2025 tax bill and support their favorite causes. The incentives are aligned: thoughtful year-end gifting in 2025 can help clients lock in deductions that might be harder to claim in future years, all while doing good.

Consider Giving Strategies for the 2025 Giving Season

Given the upcoming shifts, what strategies should advisors and their clients consider during this year’s giving season? Below are key charitable giving moves to review before 2025 ends that can enhance tax benefits and philanthropic impact:

Pull Forward Large Gifts into 2025

If your clients intend to make significant charitable donations in the next few years, it may be wise to bunch those gifts into 2025. By pulling forward planned donations, they can maximize deductions now – before the 0.5% AGI floor kicks in.

For example, rather than giving a set amount each year for the next three years, a client could donate the combined sum in 2025 to claim a larger itemized deduction. This strategy ensures none of their generosity gets lost under the future AGI floor, and it leverages the temporarily expanded SALT cap to help clear the itemization threshold. In 2026, the client may then opt for the standard deduction (when deductions become less favorable) or rely on the DAF to distribute funds to charities. In essence, bunching charitable contributions into 2025 can yield a one-time tax windfall while still fulfilling multi-year giving goals. Just be mindful of contribution limits (e.g. 60% of AGI for cash gifts, 30% for stock/property), though carry-forwards are available for excess amounts. Advisors should review each client’s projected 2025 vs. 2026 tax situation to determine if accelerating gifts makes sense.

Donate Appreciated Assets (Tax-Gain Harvesting)

Year-end is also a great time for tax gain harvesting – encouraging clients to donate highly appreciated assets instead of cash. Gifting appreciated stock, real estate, or other investments directly to charity (or a donor-advised fund) lets your client avoid the capital gains tax they’d owe if they sold the asset, yet still claim a charitable deduction for the full fair market value of the asset. This can be a double win: the client satisfies charitable goals and also sidesteps a tax hit on embedded gains.

For instance, a client with stock that has doubled in value can donate the shares to a donor-advised fund (DAF), rather than selling them – they won’t pay capital gains on the appreciation, and they get a deduction equal to the stock’s current value (usually deductible up to 30% of AGI for securities).

This strategy pairs nicely with year-end tax-loss harvesting: clients can sell some losing investments to realize losses (offsetting other gains) while gifting winning assets to charity, effectively rebalancing the portfolio in a tax-efficient way. Beyond the tax savings, donating assets allows clients to give more to charity than they might after paying taxes on a sale. Advisors should work with clients’ tax professionals to identify ideal assets for charitable gifting – often those with low cost basis and long-term appreciation – and initiate transfers well before December 31 (since processing donations of stock or real estate can take time).

Leverage Donor-Advised Funds (DAFs)

Donor-advised funds have become an increasingly popular vehicle to facilitate the above strategies and simplify charitable giving. Industry-wide, DAFs are booming – in fact, assets in donor-advised funds have roughly tripled since 2008, and there are now over 2 million DAF accounts in the United States, as AssetMark’s Chief Wealth Solutions and Strategy Officer David McNatt recently noted. The appeal of DAFs is that they let clients contribute now and decide later which charities to support. In practice, your client can make a large charitable donation to a DAF in 2025 (locking in the tax deduction immediately), and then recommend grants over months or years to various charities at their leisure. This “give now, grant later” flexibility is ideal for bunching gifts ahead of 2026 – the client can capture a big 2025 deduction by contributing to a DAF, even if they haven’t pinpointed all the recipients yet. Meanwhile, the donated assets in the DAF can be invested and potentially grow tax-free in the interim, expanding the charitable impact.

Importantly, DAFs can also help unlock illiquid, appreciated assets, such as real estate, concentrated or restricted stock, and closely held business interests, by accepting them as contributions, liquidating when appropriate, and converting them into a diversified, liquid charitable giving vehicle. For advisors, that means an off-platform, highly appreciated asset can effectively transition into a managed, on-platform charitable account, aligning portfolio, tax, and philanthropic objectives while creating economic benefits for both the client and the advisor.

DAF providers (including AssetMark’s new charitable program) handle all the recordkeeping and IRS compliance, making giving far simpler – one donation receipt for tax purposes, but the ability to support multiple causes over time. They also relieve smaller charities of the administrative burden that can come with large or complex direct donations. Put differently, an IRS-approved but resource-constrained nonprofit may struggle to accept certain types of gifts; the DAF sponsor does the “heavy lifting” (due diligence, processing, liquidation) so the end charity can receive straightforward cash grants and focus on impact.

By using a DAF, clients also avoid the limitations of the new above-line deduction (since DAF gifts won’t count for that $1k/$2k non-itemizer break); instead, they maximize deductions through bunching and itemizing. In short, a donor-advised fund is a powerful tool for year-end planning: it enables large up-front gifts in 2025 to maximize tax benefits, while preserving the client’s freedom to distribute funds to charities thoughtfully in the future. (As a bonus, a DAF can act like a “charitable savings account” that encourages ongoing philanthropy – clients can involve their family in grant decisions and build a charitable legacy together.)

Make the Most of Year-End: Help Clients Act Now

With 2025’s changes on the horizon, financial advisors have a unique opportunity and responsibility to help clients act before the year is over. Now is the time to reach out and review each client’s philanthropic goals and overall tax picture. Which causes are most important to them? How much were they planning to give in the next few years? By identifying those intentions, you can then implement the strategies above – from bunching donations and funding DAFs to gifting stocks – tailored to the client’s situation. The ultimate aim is to maximize impact and minimize taxes, allowing clients to give more meaningfully while the current tax rules still apply.

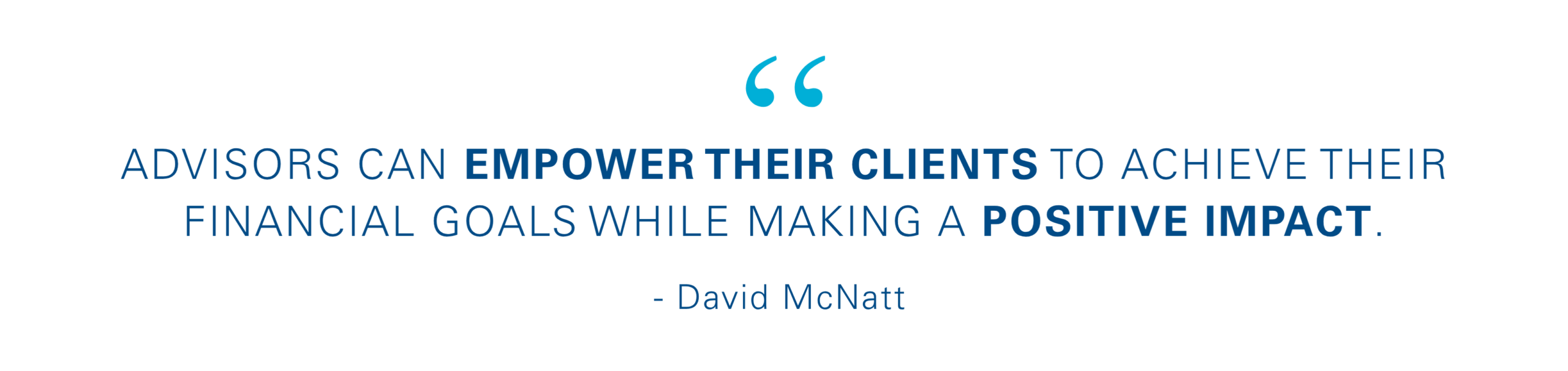

As David McNatt has emphasized, weaving charitable planning into wealth management is a win–win for advisors and clients alike: “By seamlessly integrating philanthropy into financial plans, advisors can empower their clients to achieve their financial goals while making a positive impact on the causes they care about.” In practical terms, this means guiding clients to tax-smart giving strategies that not only reduce their tax liabilities but also deepen client engagement and help fulfill their personal values.

Don’t wait until it’s too late. Proactively encourage your clients to take advantage of this year’s favorable tax environment for charitable giving. Help them review and refine their philanthropic plans now, before the hectic final days of December. Whether it’s opening a donor-advised fund, accelerating a pledged gift, or donating appreciated investments, these moves can significantly boost a client’s financial and charitable outcomes. By acting in 2025, your clients can lock in deductions and amplify their generosity, putting them in a strong position when the new rules take effect in 2026. In the end, facilitating these year-end giving strategies not only benefits your clients’ tax bills and beloved charities, but also reinforces your role as a trusted advisor who helps clients expand their impact in every sense. Now is the perfect time to collaborate with your clients on making their year-end giving as impactful and tax-efficient as possible.

If you’re interested in how the AssetMark Charitable Donor-Advised Fund could empower your clients to give back more effectively and make a lasting impact on the causes they hold dear this giving season, contact AssetMark today.

©2025 AssetMark, Inc. All rights reserved.

8546090.1 | 11/2025 | EXP 11/30/2027