We’ve reached the end of the third quarter and it’s time to assess the markets. What were some of the big drivers and takeaways? Let’s check in.

While the third quarter of 2025 was a bit less volatile than the second, investors continued to show confidence in the U.S. market, despite the ongoing economic uncertainty.

If you held a globally diversified 60/40 portfolio (60% global stocks mixed with 40% global bonds), you likely saw gains of around 4.8% compared to the 8.8% you saw in the second quarter. Here are some key economic and market indicators that factored in last quarter:

Stocks Continued Their Steady Climb

While the S&P 500 didn’t quite reach the second quarter’s 10.85% jump, the third quarter continued to show growth with a return of 8%. Fed rate cuts and strong earnings from AI-driven spending in mega-cap tech contributed to the Russell 2000, Nasdaq, S&P 500, and Dow Jones all reaching record highs, slightly outperforming international markets.

Fed Cuts Interest Rate by 25 Basis Points

The U.S. Federal Reserve cut the benchmark interest rate from 4.5%-4.25% to 4.25%-4% in mid-September. This was the first cut of the year and was highly anticipated. The Fed signaled that there could be two more rate cuts on the horizon for 2025 as it continues to balance interest rate cuts with economic growth, inflation concerns, and a softening job market.

Labor Market Growth Stalls

Through Q3, the job market has stalled and the unemployment rate rose to 4.3%. The demand for workers continued to fall due to AI adoption and policy changes.

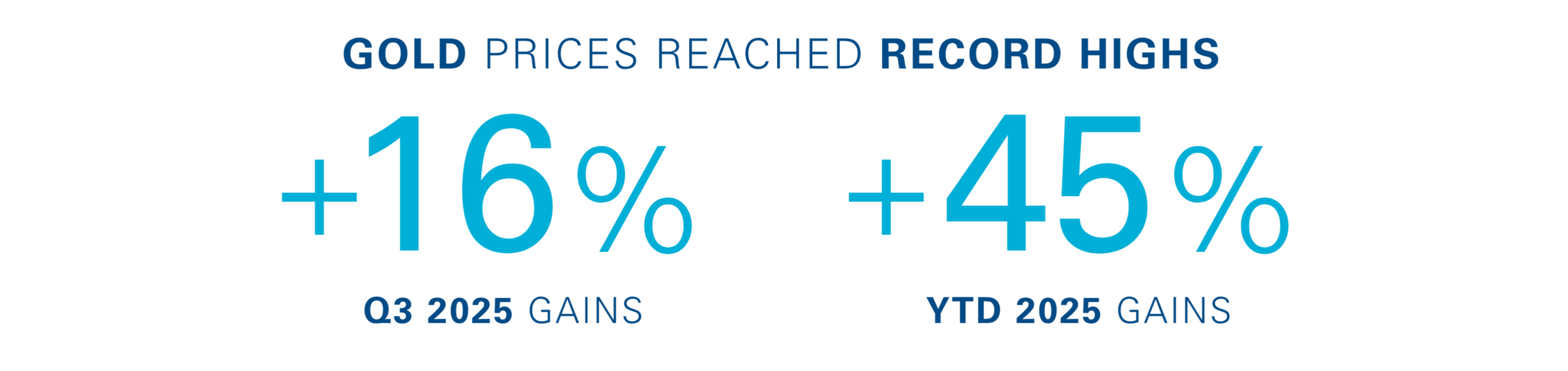

Gold Shined as Oil Faced Volatility

Gold continued its momentum, rising another 16% (Bloomberg Gold index), bringing the year-to-date gain to an astounding 45%. Gold reached record highs, driven in part by economic uncertainty. Oil prices experienced volatility that erased their early Q3 gains, stemming from softening demand and rising global supply.

GDP Continued Strong Growth

The U.S. GDP increased at an annualized rate of 3.8% in the second quarter due in large part to robust consumer spending and steady demand across services and durable goods. This rebound came from the economy contracting 0.6% in the first quarter.

Global Markets Held Strong

International markets also posted strong gains in the third quarter with the MSCI All World ex-U.S. index showing gains of 7.0%. Asia showed the strongest gains with MSCI China index rallying 21% driven combination of policy support, economic stabilization, and improving investor sentiment and MSCI Japan index returning more than 8.2%, fueled in large part by favorable currency moves, policy support, and tech strength. European markets showed modest positive gains supported by easing inflation and improved consumer sentiment across the eurozone.

Bond Markets Continued to Hold Steady Despite Uncertainty

Sentiment moved to optimism due to Fed rate cuts sending bond yields lower and prices higher.

Key Takeaways from the AssetMark Investment Team

Christian Chan, Chief Investment Officer

We saw a “risk-management” interest rate cut in September. Unemployment is still low, but there are signs of softening ahead. That’s something investors and advisors should expect to impact the fourth quarter.

The Big Beautiful Bill will likely give the economy a boost, including a bigger standard deduction for many households and investment incentives for businesses. That modest tailwind will extend over the next couple of quarters.

We’re entering a seasonally soft period for stocks. If growth continues to be solid, the Fed may not continue with additional rate cuts.

Kezia Samuel, Chief Market Strategist

U.S. stocks soared to record highs in the third quarter on renewed artificial intelligence enthusiasm. The U.S. wasn’t the only market that appreciated AI. Emerging market equities in the China also benefited as investors looked to China for other AI opportunities.

Interest rate sensitive small cap stocks outperformed their larger counterparts for the quarter. The outperformance was driven by the immediate benefit to small caps from lower borrowing costs due to their higher dependence on variable-rate loans and bank debt, enhancing their profitability and financial flexibility.

Gold is one of the best-performing investments for the year. Foreign central banks are reducing their treasury allocations and buying more gold. They now hold more gold that the U.S. Treasuries, something that we haven’t seen since 1996.

Zoë Brunson, Chief Investment Strategist

Avoid complacency. It’s always easier to be complacent and put things off if everything seems to be working today. But that could mean leaving biases in portfolios that are unintended.

- Avoid sitting on cash. Interest rates cuts are lowering the return on cash, and it could mean not meeting your financial goals.

- Don’t think long-term bonds will deliver in a falling rate environment. Focus on active management instead.

- Consider reducing exposure to U.S. mega-caps through diversification of style and geography. Diversifying away from U.S. stocks during times of dollar weakness can provide additional sources of return.

Don’t be like a student who leaves their homework to the last minute. Be disciplined and take the time now to make sure portfolios are diversified and aligned with long-term and short-term goals.

What to Watch For in Q4 as We Wrap Up 2025

The end of 2025 will likely continue to bring unexpected changes. As you prepare for the rest of the year, several key factors could influence the economy and markets:

- Federal Reserve policy and interest rates: How will the market respond if the Fed doesn’t cut rates?

- Inflation trends: Will the September interest rate cut increase inflation?

- Corporate earnings: Is mega-cap tech going to consistently post strong earnings as AI adoption continues?

- Labor market: Is the job market going to continue to soften, and how could that affect hiring, wages, and consumer spending going into the holiday season?

- Geopolitical tension: As trade negotiations unfold amid ongoing tensions, will there be further disruptions to commodities and supply chains?

- International markets: Will we see continued shifts in the global market due to currency moves and policy changes?

- Elections: With the 2026 midterm cycle approaching, will political developments impact fiscal policy and investor sentiment?

- Government shutdown: Will the October 1st shutdown be resolved quickly? Or will a prolonged stalemate begin to affect GDP growth, delay federal spending and affect market confidence?

And, as always, stick to a solid financial plan, keep your portfolio diversified, and stay focused on your long-term goals. That’s how you stay ready and flexible, no matter where the markets go next.

Important Information

This is for informational purposes only, it is not a solicitation, and should not be considered investment, legal or tax advice. The information has been drawn from sources believed to be reliable, but its accuracy is not guaranteed and is subject to change.

Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results.

AssetMark, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission.

©2025 AssetMark, Inc. All rights reserved.

8464452.1 | 10/2025 | EXP 10/30/2027