Key Takeaways

- High-net-worth clients often expect support beyond portfolio management, including help coordinating wealth transfer, estate planning, trust services, financial planning, and investment management.

- Cerulli research suggests high-net-worth relationships can be fluid, with many investors adding or changing wealth relationships as their needs evolve.

- Next-generation relationships matter. Advisors who build connections before assets transfer may be better prepared for one of the most vulnerable moments in the client relationship.

The opportunity for financial advisors has never been more compelling. According to Cerulli, U.S. household net worth reached a record $90 trillion in 2024, with approximately 3.4 million high-net-worth households commanding $49 trillion in financial assets. That concentration signals where the most meaningful advisory work may be headed.

But capturing that opportunity requires more than investment management expertise. As wealth grows, complexity grows with it, and HNW clients are increasingly aware of the difference between an advisor who manages a portfolio and one who orchestrates a financial life.

These clients have expanded and interconnected needs: wealth transfer strategies, estate planning, trust services, tax efficiency, charitable giving, and long-term planning that evolves with their goals.

These needs drive the HNW client migration.

The three phases of HNW client migration

High-net-worth client relationships often move through three phases: searching, consolidating, and transferring. Each phase creates a risk, but more importantly, potential opportunities for advisors who can deliver these services with a coordinated strategy built around the client’s full financial picture.

Phase 1: Searching for services

Many high-net-worth investors begin by looking for services beyond investment management and basic planning. They may need help coordinating estate conversations, tax planning discussions, lending needs, private market access, charitable giving, or family wealth education.

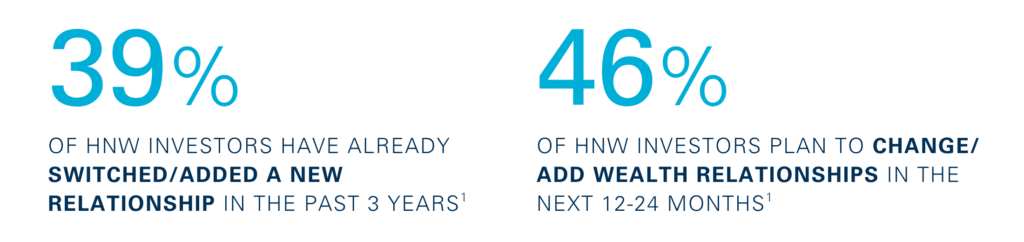

Because one advisor or institution may not provide everything they need, these clients often add relationships over time. They may keep one advisor for investments, consult another professional for tax-sensitive planning, work with an estate attorney, and use separate providers for banking or trust services. This movement is already visible. Cerulli found that 39% of high-net-worth investors have switched or added a wealth relationship in the past three years, and 46% plan to change or add a wealth relationship in the next 12 to 24 months.

Searching for services creates vulnerability for advisors who are not prepared to discuss wealth management more holistically. However, this search phase can create openings for advisors who can clearly explain their service model and show how they support more complex client needs.

Phase 2: Consolidating for simplicity

Multiple relationships can be useful at first. Over time, they become hard to manage. Clients may grow tired of repeating information, coordinating separate conversations, disconnected advice and making sure each provider understands the full picture.

As complexity increases, simplicity becomes more valuable. According to Cerulli, 58% of affluent investors expressed interest in consolidating all investable assets with a single institution.

For advisors, this phase rewards preparation. A clear service model, documented planning process, and strong professional network can help show that your practice is ready to support more advanced needs. The risk is claiming that you can do everything. The goal is to show clients how you help bring the right pieces together in a way that supports their unique journey.

Phase 3: Transferring wealth

The final phase often occurs when a wealth transfer takes place after the death of the account owner.

This is a critical moment. If the next generation does not have a relationship with the advisor, sees their process as complex, or feels that you do not understand their situation, assets may leave. Heirs may already have their own advisors, different expectations, or little understanding of the planning work that came before the transfer. The retention risk is meaningful. Cerulli found that only 27% of affluent investors expecting an inheritance planned to keep the wealth advisor who managed those assets, and only 20% of affluent investors who received an inheritance kept the original wealth advisor.

Advisors can prepare by building relationships earlier. That may include inviting adult children into appropriate planning conversations, helping clients communicate family goals, or offering education around inheritance, philanthropy, or financial decision-making.

These conversations require care and waiting until a transfer occurs may be too late. Advisors who respect privacy, family dynamics, and the estate planning process across generations are better positioned to maintain assets when their original client passes.

What advisors can do now

Start by reviewing three areas of your practice:

- Which services high-net-worth clients are asking for beyond investment management and financial planning

- How do those services fit together in a holistic wealth management experience, and

- Where might it be appropriate to build relationships with the next generation before a transfer event occurs.

High-net-worth clients are often looking for clarity, coordination, and confidence in the people supporting their financial lives. Advisors who prepare for each phase of the migration may be better positioned to keep those relationships strong as client needs become more complex.

The high-net-worth client migration is not only about retaining assets. It is about being ready for the broader expectations that often come with wealth.

Sources:

- PwC High Net Worth Investor Survey, December 2022

- The Cerulli Report | U.S. High-Net-Worth and Ultra-High-Net-Worth Markets 2024

©2026 AssetMark, Inc. All rights reserved.

8972731.1 | 06/2026 | EXP 06/30/2028