“May you live in interesting times” is usually taken as a good-natured sentiment. That is until things start to get interesting in a bad way. Economic volatility and market downturns certainly catch the attention of advisors and investors alike, for all the wrong reasons. Adding to the uncertainty? Not all market declines are the same–duration, intensity, impact, and scope are key differentiators–compounding an already confusing situation.

So, let’s look at the different types of market declines, provide some historical perspective, and discuss actionable steps financial advisors can take to ease client trepidation…and perhaps build their businesses in the process.

Read all of this 2-part series: How to Prepare Your Firm for a Market Downturn or Recession.

What is a Market Downturn?

Thanks to the internet and 24-hour news cycle, there’s no shortage of descriptions of a market downturn. The number of pundits willing to opine on the topic is impressive, too. Simply put, a market downturn occurs when securities tracked by a market index fall in price. The causes and duration vary. But the primary investor reaction is consistent: anxiety.

What is a Bear Market?

Essentially, a bear market is a prolonged and somewhat steep market downturn. It occurs when stocks fall 20 percent from a recent high. For all the optimists out there, a bull market starts when the market gains 20 percent from market lows.

What is a Recession?

The common definition of a recession is two consecutive quarters of negative Gross Domestic Product (GDP). Other criteria include declines in real income, employment rates, retail sales, and consumer spending. A recession’s negative impact on Americans across economic classes is its defining trait.

What is a Stock Market Crash?

A stock market crash is a drastic, often unforeseen, drop in stock prices. Most market crashes are short bursts of market instability leading to dramatic downturns. Some last a single day, others much longer. In either scenario, investors suffer heavy losses.

The occasional recession might make history books. Stock market crashes always do. That’s because they are traumatic, and they are rare. Since 1929, there have been 26 bear markets in the S&P 500 index, with an average decline of almost 36%.

What Causes a Market Downturn?

As we saw above, the “what” of market downturns is fairly consistent. The “why” is more complicated. Recurring factors emerge time and again, including unemployment, monetary policy, inflation, geopolitical turmoil, and natural disasters. Sometimes, unique scenarios are the culprit:

- The 2000-2001 dot-com crash was the result of both Y2K preparation and overvalued tech company stock prices not aligning with company fundamentals.

- 2020 saw “pandemic” added to the trigger list:

Between Feb. 12, 2020, and March 23, 2020, the Dow lost 37% of its value. By the middle of March, the panic was rising. As the US went into lockdown mode, over 20 million jobs were lost, businesses closed, and the virus continued its spread. Investors watched as their retirement savings lost 30% in two weeks.

Cybersecurity, cryptocurrencies, climate change, and more will no doubt come into play going forward. Additionally, with the interconnectedness of world economies, businesses, and stock markets, a small ripple felt across a sector or across the globe can cause a multiplying domino effect impacting entire markets. Being positioned for a downturn is key to an investor’s potential for long-term success.

A Brief History of Market Downturns

Most market downturns come and go, generating a period of uncertainty but typically leaving investors with little long-term financial damage. If we look at the big picture, we see that market loss is fairly infrequent: In the 92 years between 1929 and 2021, bear markets comprised only 20.6 years. In other words: stock markets generate gains 78% of the time.

And, when large market downturns have occurred, they have generally been followed by periods of impressive growth (on average 114% in the typical bull market):

THE WORST YEARS EVER FOR THE U.S. MARKET

| YEAR | S&P 500 | REASON | NEXT YEAR | 3 YEARS | 5 YEARS |

| 1930 | -25.1% | Great Depression | -43.8% | -23.0% | 11.6% |

| 1931 | -43.8% | Great Depression | -8.6% | 35.4% | 162.1% |

| 1937 | -35.3% | 1937 Crash | 29.3% | 14.2% | 18.7% |

| 1940 | -10.7% | WWII | -12.8% | 30.0% | 110.2% |

| 1941 | -12.8% | WWII | 19.2% | 77.4% | 120.6% |

| 1957 | -10.5% | 1957-58 Recession | 43.7% | 61.6% | 86.6% |

| 1973 | -14.3% | 1973-74 Bear Market | -25.9% | 25.7% | 24.5% |

| 1974 | -25.9% | 1973-74 Bear Market | 37.0% | 57.8% | 99.2% |

| 2001 | -11.9% | Dot-Com Crash | -22.0% | 10.9% | 34.4% |

| 2002 | -22.0% | Dot-Com Crash | 28.4% | 49.0% | 81.7% |

| 2008 | -36.6% | Great Financial Crisis | 25.9% | 47.6% | 126.1% |

Of course, past performance is no indication of future results.

7 Tips for Navigating Volatile Markets with Your Clients

A 2020 Hartford Funds survey found that while almost all financial advisors say they’ve discussed bear market preparations with their clients, only 43% of surveyed clients recall the conversation. So, advisors shouldn’t assume clients are prepared for a downturn.

Navigating a market downturn of any kind is not about luck, and it’s not about hoping for the best. It’s also not always about numbers. As a financial advisor, your job is to look beyond the AUM and portfolio value to see the people behind those accounts, and the goals, dreams, and legacies embedded in their account values. Stay engaged, make yourself available, anticipate questions (and have the answers), help them weather this storm, and be ready for the next one.

Tip 1: Communicate.

Investors look to financial advisors to be the objective, informed voice of reason when a kneejerk “sell” reaction is their first instinct. Call your clients rather than wait for them to call you. Proactive communication reinforces to your clients that they are top of mind for you and that you are on top of the situation. Have prepared templates at the ready, and ensure your CRM is always up to date, so you can get in front of clients quickly.

Tip 2: Educate.

In addition to guidance, clients want to understand what is going on, why it is going on, and what they can expect in the weeks and months ahead. Offering educational materials such as whitepapers, market commentaries, and fact sheets not only puts your clients at ease but also positions you as an expert and gets ahead of potential questions.

Tip 3: Provide Perspective

Market volatility and economic uncertainty are not new. Share historical data with clients to remind and reinforce that market downturn is part of investing. Run hypothetical performance calculations, such as a Monte Carlo simulation, to demonstrate the probability of outcomes over time. Discuss the power of diversification and how it protects investments during market cycles. Last but certainly not least, remind them of their long-term plan.

Tip 4: Go Over the Numbers.

Volatile markets may lead clients to rethink their risk tolerance, especially if they are close to retirement. Reduce client anxiety by discussing where they are invested and why, and help them understand potential solutions to offset near-term impacts. For example, discuss a possible increase in cash reserves and income-generating investments, and lower-risk solutions for clients concerned about cash flow. Discuss cash management /debt reduction solutions where necessary. If appropriate, discuss tax-loss harvesting or a Roth conversion. Help clients feel a little more in control.

Tip 5: Empathize.

Clients may feel vulnerable when they don’t understand what is happening and may fall victim to a “what if” spiral. Acknowledge their anxiety and offer tangible coping skills. Reiterate that ups and downs are inherent in the market. Also, have a conversation that includes elements that are not related to money, investments, or wealth. Empathy and expertise are a win-win combination when working with clients who often want to just talk through their fears.

Tip 6: Target Your Outreach.

There’s no “one-size-fits-all” conversation during market downturns. How you engage retirees should differ from how to interact with Millennials. High-net-worth clients have different expectations from small business owners. A seasoned investor may not require the assurances needed by someone experiencing their first market downturn. Review your client segmentation and marketing and client retention campaigns, so that the right content reaches the right clients.

Tip 7: Hold Family Meetings.

Offer your clients the opportunity to invite whomever they want—whether significant others or all family members—to a meeting. This allows each individual time to express how they think about money and investing, what their goals are, and how they can work together to achieve them. These meetings may also introduce you to the next generation and allow you to showcase your skills and expertise. If you’re working with AssetMark, ask about the Family Preparedness Kit and the white-labeled client-facing Family Preparedness Deck.

Weathering a Bear Market: 2022 and Beyond

An important part of a financial advisor’s job is to prevent clients from acting out of fear or emotion. However, that’s not an easy proposition as clients continue to see red–literally–when reviewing their portfolio performance. Intellectually, clients understand that selling low is costly. Emotionally, it’s perceived as a defense mechanism that will avoid further loss. How can you engage clients in a way that addresses their fears, yet won’t compromise their financial future? Discuss time-tested approaches that have served investors well over time.

Navigating Volatile Markets

While “sit tight” is a reasonable approach, it’s not the only one. Put volatility to work. Consistently investing over time, via dollar-cost averaging can minimize the impact of market movements. Another “set it and forget it” option: Maxing out 401k and HSA contributions–especially, to take advantage of a company match.

Staying Invested During Volatile Markets

It’s About Time. Not Timing.

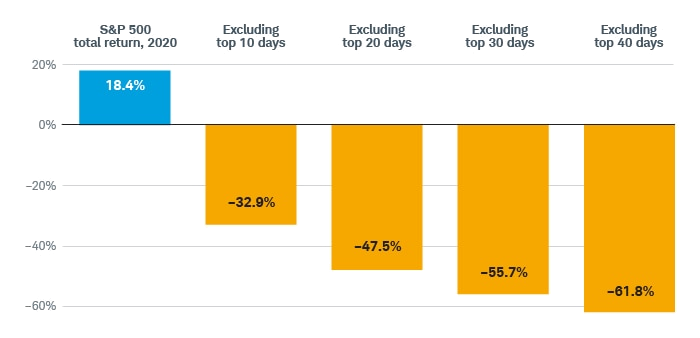

Just as investors can’t avoid volatility, they can’t time the markets consistently. As seen below, missing just a handful of top-performing days can have a devastating effect on returns.

Source: Schwab Center for Financial Research with data from Standard and Poor’s.

Another reason to stay invested during volatile markets? In the last 20 years, half of the S&P 500 index’s strongest days occurred during a bear market.

Recession Investment Strategies

Often in a recession, there’s no “good” place to invest. But some places are better than others. Consumer staples are a relatively safe haven in recessionary times. People always need food, utilities, and healthcare. Dividend-paying stocks are another smart choice to keep income flowing. Staying invested and buying low are proven options as well, as is positioning portfolios to participate in the recovery. It all depends on a client’s tolerance for risk, their time horizon, and their goals.

So, What Now?

Market downturns, volatility, and recessions all pass in time. According to The National Bureau of Economic Research, we’ve had nine recessions since 1960, lasting an average of about a year.

But when you and your clients are in the midst of such uncertainty, it can be difficult to see the light at the end of the tunnel.

It’s important to remind clients that volatility is normal. That risk and reward are two sides of the same coin. Encourage them to keep their eyes on the prize and not be discouraged or waylaid by a temporary situation.

As for you, be sure to ask your outsourcing provider for materials to support you and your clients.

If you’re working with AssetMark, ask about our Market Volatility Tool Kit which provides educational materials that you can send to your clients, email and video templates, and white-labeled resources that you can add your logo to and share with your clients.

If you’d like to learn more about these AssetMark services, as well as other support capabilities available from AssetMark, talk to your AssetMark consultant.