More than half of Gen Z and Millennials wish they had made different investment decisions in the last year. With half of Gen Z already venturing into the world of investments and a fifth of them wanting to learn how to invest, it would seem like an opportune moment for financial advisors to swoop in as the heroes to guide young people as they step into the world of investing and financial planning.

But before you don that cape, take a few moments to listen to The Modern Financial Advisor podcast, where host Mike Langford and Natalie Wolfsen, former CEO of AssetMark, dig into the topic of next-gen investors and what they expect from their financial advisor relationship.

Here we’ll bring you some background information on the topic and some of the highlights from their conversation.

How old are young investors?

The investor landscape is changing. Millennials are now in their thirties—the oldest of whom is 40—and they’re having kids and making larger financial decisions. Gen Z is in their teens and twenties and already starting to invest.

So, if Gen Z is still in their teens and twenties, is it too early to consider them active investors? You’re probably wondering: What percent of Gen Z are even investing? More than half of Gen Z already hold some type of investment, partially due to exposure through social media and investing apps, high school clubs like the Young Investors Society, or access to parent-supervised accounts.

As for the rest who haven’t jumped in yet, the majority say they don’t know where to start investing. Those who have started rely primarily on online videos to learn about the world of investment.

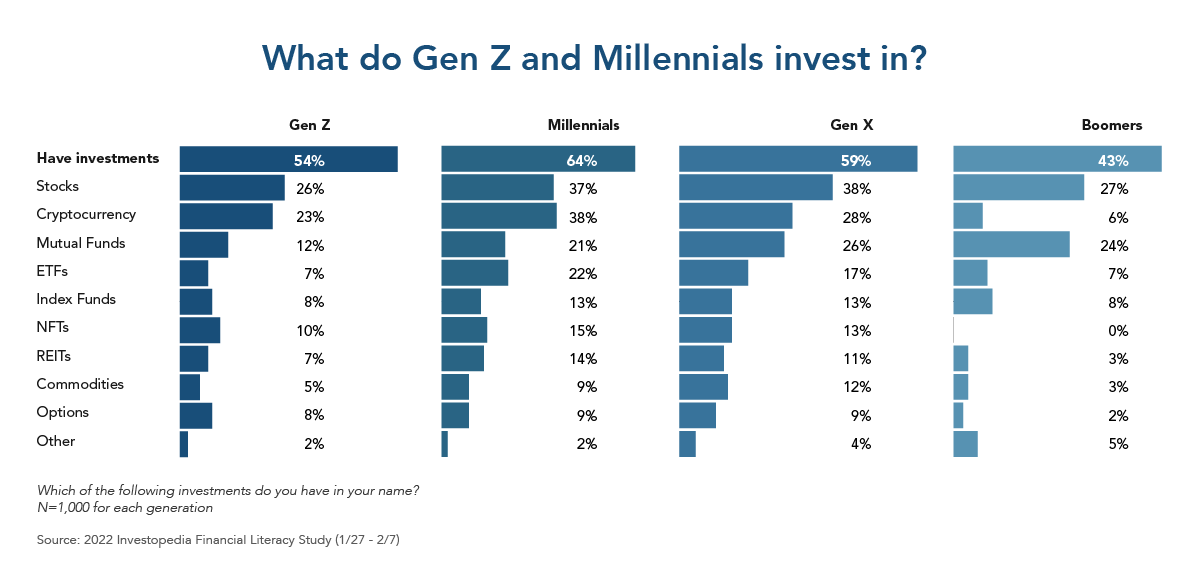

What do young investors invest in?

The general assumption is that young investors are driving the bitcoin and NFT craze and have little to no interest in traditional investment products or the stock market. However, an early 2022 Investopedia study found that Gen Z and Millennials are indeed investing in cryptocurrency, yes, but also stocks, mutual funds, ETFs, and more.

And what’s the most popular investment for a young investor? Stocks beat out cryptocurrency for Gen Z, and for Millennials, stocks are a close second behind cryptocurrency.

How are Gen Z and Millennial investors different?

Gen Z started investing at a younger age compared to Millennials and they seem to already have a higher level of financial literacy beyond the basics of personal finance: best practices of credit cards, interest rates, and compound interest. These younger investors are learning about financial markets, setting financial goals and investment strategies, and they understand the power of compounding. As a result, some are even beginning their retirement planning.

Wolfsen explains: “Sometimes people bundle Millennials and Gen Z together. They could not be more different. Their experiences have left them in completely, almost opposite spaces.

“Millennials, they had two big market dislocations. They’re categorized by an environment of high polarization. They’re very hesitant with the market and very hesitant to take advice. They look towards their networks. They look to their communities for advice. They got into investing really late as a result of their experience.

“And then, there’s Gen I. Gen I is the 15% of investors who started investing in 2020. With a median age of 35, Gen I is younger than those who began investing before 2020 whose median age is 48, but this new generation of investors spans all age groups. There is a great study on generation investors. 82% of those new investors want advice. They’re seeking advice. They’re seeking out the markets. They’re really interested in investments. Not just traditional investments, but NFTs and digital assets. These are highly experimental, highly risk-seeking investors. Very different from Millennials, in my view.”

“Millennials have seen market corrections. They’ve seen a real estate crash. A bubble. They’ve seen a Great Recession, where many of them were starting their career off and getting their butts kicked. Life is dramatically different. That shapes your worldview,” adds Langford.

Wolfsen agrees, “It’s absolutely true. These, I’ll say, younger investors … they’re just very different. And so, as an advisor or as someone who serves advisors like AssetMark, we have to treat them differently.”

How are Millennial and Gen Z investors the same?

Wolfsen explains the common thread between Millennials, Gen Z, and even Gen X: “As we age, there are certain things that change about us. We’re more concerned about the long term, more concerned about leaving a legacy, and more concerned about our kids’ education. More concerned about saving versus adventures. These are the types of things that change with age, regardless of generation.

“Even so, these younger generations are quite different from the standard investor profile. All of us in the industry need to embrace it. They want to make an impact and they view their money as a way to vote. They want that kind of impact on the world.

“They care about the environment. They care about inclusion. They care about creating a better world for the next generations than the one they inherited. And it’s one of their primary decision factors.

“And it’s fantastic. It’s a fantastic thing that the Millennials and Gen Z share. And I would argue Gen X too. We’re very focused on making an impact.”

If investors are changing, how is the financial advisory industry changing?

When investors change, naturally, the industry that supports them and gives them advice will, too. Wolfsen sees two important ways that things have already begun to change: “I think two important things have changed. One is, there was a time, maybe even just four or five years ago, where people believed you either invested for impact or you invested for returns. And so, you’d be giving up returns if you invested for impact.

“That has been debunked with ESG research. That belief has been disproven. And that’s an important thing. For those of us who were thinking, ‘I can’t afford to invest for impact,’ that’s incredible information to have.

“The second thing that I think has changed is … Not only do consumers have more information, but they also have the digital tools that help them interpret it. No more sitting with an investment professional and hearing about market volatility or standard deviation or the beta of your stock. We can all go online and chart that stock and see how it’s doing relative to the benchmark. Understand the terminology in a very easy-to-digest way. And so, what’s happened in the industry is investors’ expectations have gotten higher, as it relates to the communications they have with their advisors and the tools that their advisors use.”

How will the future of the financial industry change?

We’ve already seen changes; the logical next question poses itself: will there be even more changes? Wolfsen’s answer is yes: “I think that Gen Z is creating such an opportunity for the market. I think they’re going to push us just like Millennials did. Millennials pushed us to be more digital and more interactive.

“Gen Z is going to push us to be more personalized. They’re going to push us to be thinking about portfolios and investments differently. That’s fantastic. It makes the industry better.”

Langford further pointed out that, “the demographics of America are changing from that diversity, equity, and inclusion perspective. But demographics are also changing from a generational perspective. The new wealth segment will be held with Millennials. And then, coming right behind them, Gen Z. If you’re going to have a firm that lasts for another 20 or 30 years, you must start thinking about marketing, attracting, and then serving these client bases.”

These are not just speculations. Wolfsen cited a recent study from McKinsey, “This study was saying that by 2030, 80% of investors will expect completely custom investment portfolios. That’s a huge shift.”

How can advisors better serve young investors?

Host Langford asked Wolfsen about advisors who have been in practice for decades, have several 100 million AUM, and realize that they need to start serving younger clients, some of whom are the children of their affluent or high-net-worth clients. What can a seasoned advisor do to adjust to the expectations of a new, young investor?

Advisors can do three things today:

- Upgrade the firm’s tech platform.

Digital platforms, like AssetMark’s Investor Portal, help clients stay connected to their accounts and engage with their advisors anytime from their phones. Advisors should also take the extra step to brand the portal and support their marketing ecosystem. - Be ready to talk about values, ESG, and other values-driven investing opportunities.

Four out of five investors want their advisors to talk about how their investments can reflect their personal values. Advisors need to be prepared to talk about values and integrate ESG and faith-based investments into client portfolios. - Be prepared to include digital assets in portfolios.

Digital assets, like NFTs and cryptocurrencies, are increasing in demand and edging their way into second place in investment products right behind stocks. Rather than cull “through thousands of investment options, learning about NFTs and cryptocurrency, and figuring out how to custody those solutions, advisors can outsource all that to somebody else and hold them accountable. Then, redeploy that time to serving your clients.”

To meet young investors where they’re at, advisors need to be ready to provide millennials and Gen Z the investment solutions they want, the way they want it.

Remember that study on generational investors who entered the market in 2020, “82 percent are interested in access to an investment professional to provide ongoing help and guidance.” They want your support, you just need to be ready to provide it.

Listen to this podcast on young investors

In this one-hour podcast, Langford and Wolfson talk about whether advisor fees are changing, how a financial advisor’s value proposition is transforming today with the emergence of robo-advisors, and how financial professionals can scale their businesses and be more effective with clients. Listen to the podcast to learn more.